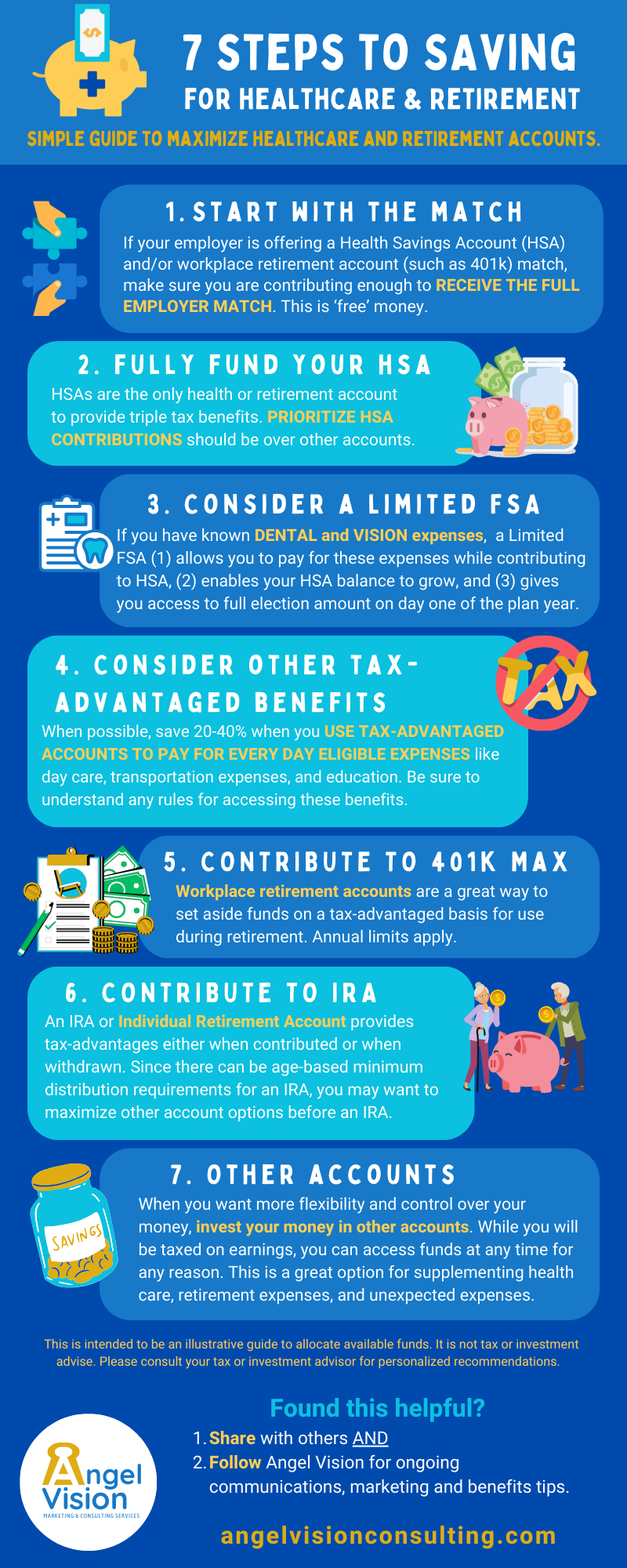

7 Steps to Saving for Healthcare and Retirement

Simple Guide to Maximize Healthcare and Retirement Accounts

Most of us have to prioritize where we allocate our money, but we often look at each decision independently. Follow these seven steps to maximize your limited dollar allocation. The steps are designed to be iterative. If you complete one step and still have money to allocate, move on to the next step. Don't worry if you are unable to complete all seven steps.

This is intended to be an illustrative guide for possible allocation of funds. It is not tax or investment advice. Please consult your tax or investment advisor for personalized recommendations.

1. Start with the Match.

If your employer is offering a Health Savings Account (HSA) and/or workplace retirement account (such as a 401k) match, make sure you are contributing enough to receive the full employer match. This is 'free' money. An HSA match is typically a set dollar amount. For example, your employer will match a contribution up to $500. Workplace retirement plans can be a little more complicate but will be based on a percent of income. Let's say your employer matches at 100% for the first 2% and 50% for the next 4%. In order to receive the full contribution, you would set your election to 6%.

2. Fully fund your HSA.

HSAs are the only health or retirement account to provide triple tax benefits. The money is deposited tax-free, grows tax-free and remains tax-free when used on qualified medical expenses. If you need to use HSA funds after age 65 for non-medical expenses, they are taxed at ordinary tax rates and offer the same advantages as any other retirement account. This is why you should prioritize HSA contributions over other account options.

3. Consider a Limited FSA.

If you have known DENTAL and VISION expenses, a Limited FSA (1) allows you to pay for these expenses while contributing to HSA, (2) enables your HSA balance to grow, and (3) gives you access to full election amount on day one of the plan year.

4. Consider other tax-advantaged benefits

When possible, save 20-40% when you use tax-advantaged accounts to pay for every day eligible expenses like day care, transportation expenses, and education. The specific options available will vary by employer. Be sure to understand what options are available and any rules for accessing these benefits.

5. Contribute to 401k Max

Workplace retirement accounts are a great way to set aside funds on a tax-advantaged basis for use during retirement. Annual limits apply.

PRO TIP: Make sure you set the percent of income appropriately to receive the employer match all year long. In 2024, you can elect a maximum of $23,000. For illustrative purposes, assume income of $100,000. If you set your contribution at 30%, you will have contributed $23,000 ten months into the year causing you to miss out on the employer match for approximately two months. If you receive bonus payments or commissions, you may need to take a closer look at how these affect your contribution rate throughout the year.

6. Contribute to IRA

An IRA or Individual Retirement Account provides tax-advantages either when contributed or when withdrawn depending on the type of IRA. Since there can be age-based minimum distribution requirements for an IRA, you may want to maximize other account options before an IRA.

7. Other Accounts

When you want more flexibility and control over your money, invest your money in other accounts. While you will be taxed on earnings, you can access funds at any time for any reason. This is a great option for supplementing health care, retirement expenses, and unexpected expenses.

Found this helpful?

- Share with others

- Follow Angel Vision on LinkedIn or Facebook for ongoing communications, marketing and benefits tips.

- Request a complimentary discovery session to see how Angel Vision can assist you with your communication, education or marketing needs.